Головна сторінка Державної податкової служби України

The only state web portal

The only state web portalof electronic services

-

State Tax Service

of Ukraine - Contacts

The only state web portal

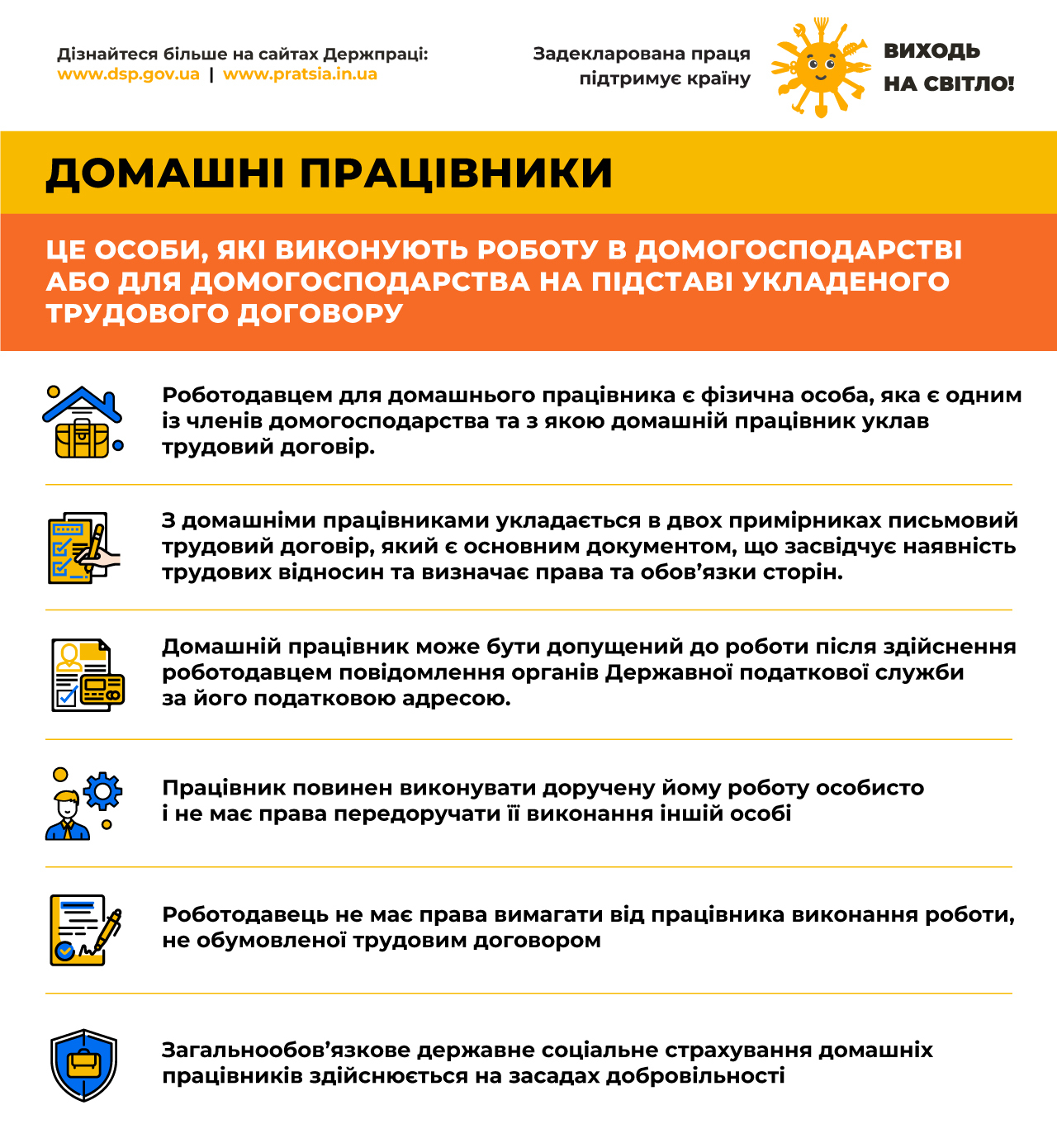

Work in or for a household may only be performed if a written employment contract is concluded between the employee and the employer is individual (one of the household members).

Employment contract:

- is concluded in two copies and is the main document confirming employment relationship and defining rights and obligations of the parties;

- employee may start work only after the employer notifies the State Tax Service’s authorities at their tax address about the employee’s employment.

Tax obligations of the employer and employee:

When officially employed, the at-home employee must independently pay personal income tax (18%) and military levy (currently 5%) on salary based on the results of annual declaration.

If the at-home employee wishes to have insurance experience, he or she must independently conclude agreement on voluntary participation in the system of obligatory state social insurance.

These deductions guarantee the at-home employee:

- inclusion of insurance experience for a future pension;

- right to receive sick leave, maternity benefits;

- social protection in case of disability.

Registration of employment relations and payment of taxes by the at-home employees remain obligatory.

Official registration of the at-home employees protects their social rights and guarantees receipt of taxes and contributions that finance state social programs.