Головна сторінка Державної податкової служби України

The only state web portal

The only state web portalof electronic services

-

State Tax Service

of Ukraine - Contacts

The only state web portal

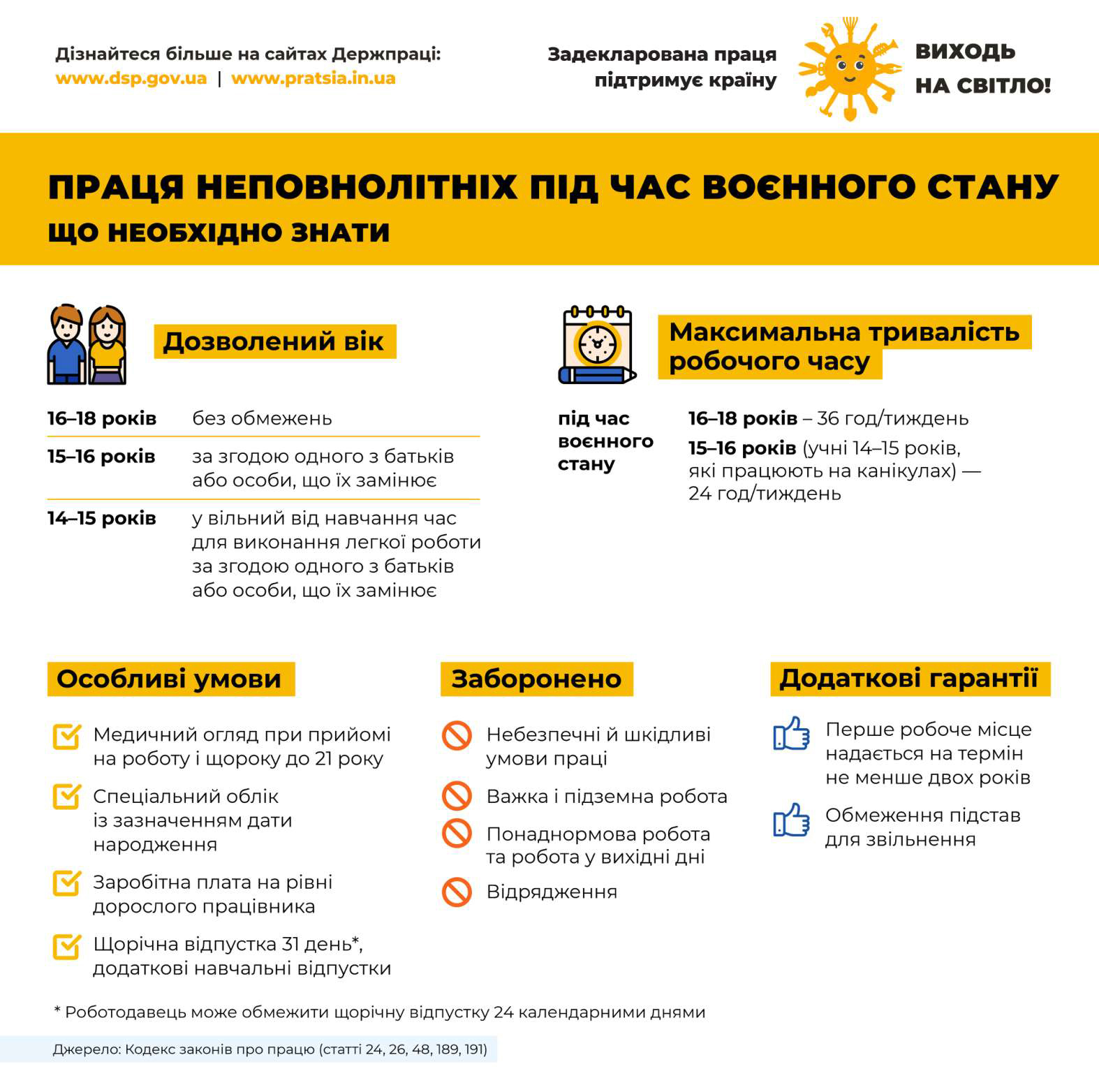

When employer officially registers a teenager, he/she pays for such minor:

- personal income tax (18%);

- 5% military levy;

- Single social contribution to obligatory state social insurance (22%).

Due to this, teenagers receive:

- salary at the level of an adult employee;

- annual paid vacation of 31 days (or 24 days at the employer’s discretion);

- social insurance and pensionable service from the first day of work.

Unofficial employment deprives them not only of sick leave and insurance protection, but also reduces their future pension provision.